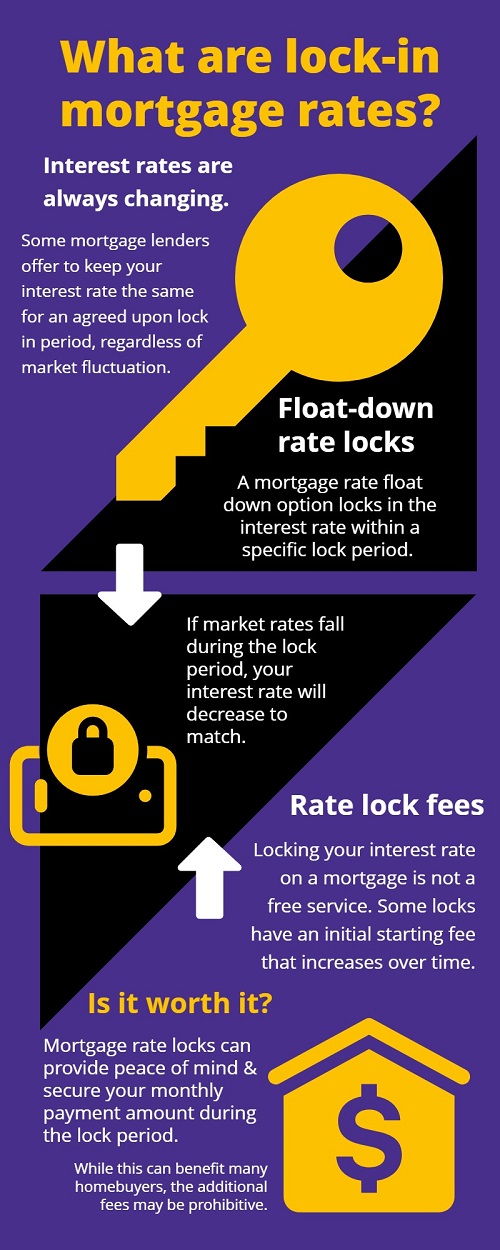

With mortgage rates constantly fluctuating, many lenders offer the ability to lock in a specific mortgage rate. These provisions keep your interest rate the same for an agreed upon lock in period, regardless of whether national rates fall or rise.

However, while a rate lock period can have its advantages, it's not the right answer for everyone. Here is some more important info about mortgage interest rates and locks for homebuyers to be aware of:

If you lock in interest rates on a mortgage loan, you can secure them from the time of approval until five days before closing. However, the lock only lasts until the end of your current loan, meaning your interest rates will no longer be locked if you refinance.

Therefore, timing your mortgage rate lock is crucial - you might even be able to get a lower rate on your second mortgage as well.

A rate lock has far fewer disadvantages than risk. An interest rate lock does not help to get the cheapest mortgages, but rather safeguards your buying power. The rate lock prevents a mortgage's interest rate from increasing and potentially pricing you out of your own home due to high monthly mortgage payments.

Various banks can lock the rates with what are called "float down" provisions. In these cases, the rate is lowered in a specific period after the loan approval. Whenever the price increases, your payment will match what you're quoted for.

While this can benefit many homebuyers, there is a risk that rates will never change in your favor. This would result in paying higher interest rates for the whole term.

Having a rate-lock may reduce your mortgage costs, but the process isn't free of charge. Generally, rate locks include a fee starting an initial amount, which increases over time. In some cases, mortgage lenders will charge a fee for extended locks. Make sure to go over the options carefully to avoid any unpleasant surprises down the road.

Should you accept a lock-in rate from your mortgage lender? Keep these factors in mind to make the best decision for your financial future.

Kim Clark started her real estate career in 1999 and shortly thereafter obtained her Broker’s license in 2002. After working for larger, corporate offices, she realized that her business and clients needed a more personalized and flexible firm. She founded Bayside Realty Consultants in 2007 offering a space of unity, collaboration and encouragement for agents and their clients. Kim specializes in the unique Cape Cod market comprised of primary, vacation and investment properties.

She says "It is great to be a part of helping make a homeowner's dreams come true". Clients and their individual needs can make things very exciting! Kimberly's enthusiasm is contagious and it has been a real asset in her successful career. She says, "Never quit. Just do what you like and the rest just falls into place." She is certified in several real estate designations including GRI, CBR, CRS, e-Certified, and a certified trainer.